NEGOTIABLE INSTRUMENTS ACT, 1881 – DETAILED NOTES

1. Definition & Characteristics of Negotiable Instruments

Definition (Section 13)

A Negotiable Instrument means a promissory note, bill of exchange, or cheque, payable either:

to order, or

to bearer

Essential Characteristics

Transferability

Freely transferable by delivery (bearer) or endorsement and delivery (order).

Title of Transferee

Transferee gets a better title (if holder in due course).

Right to Sue

Holder can sue in their own name.

Presumption

Presumed to be made/drawn for consideration (Section 118).

Certainty

Must contain a certain sum of money.

Negotiability

Must be capable of negotiation.

Unconditional

Promise/order must be unconditional.

2. Parties to Negotiable Instruments

(A) Promissory Note

Maker: Person who promises to pay

Payee: Person to whom payment is made

(B) Bill of Exchange

Drawer: Makes the order

Drawee: Directed to pay

Acceptor: Drawee who accepts liability

Payee: Receives payment

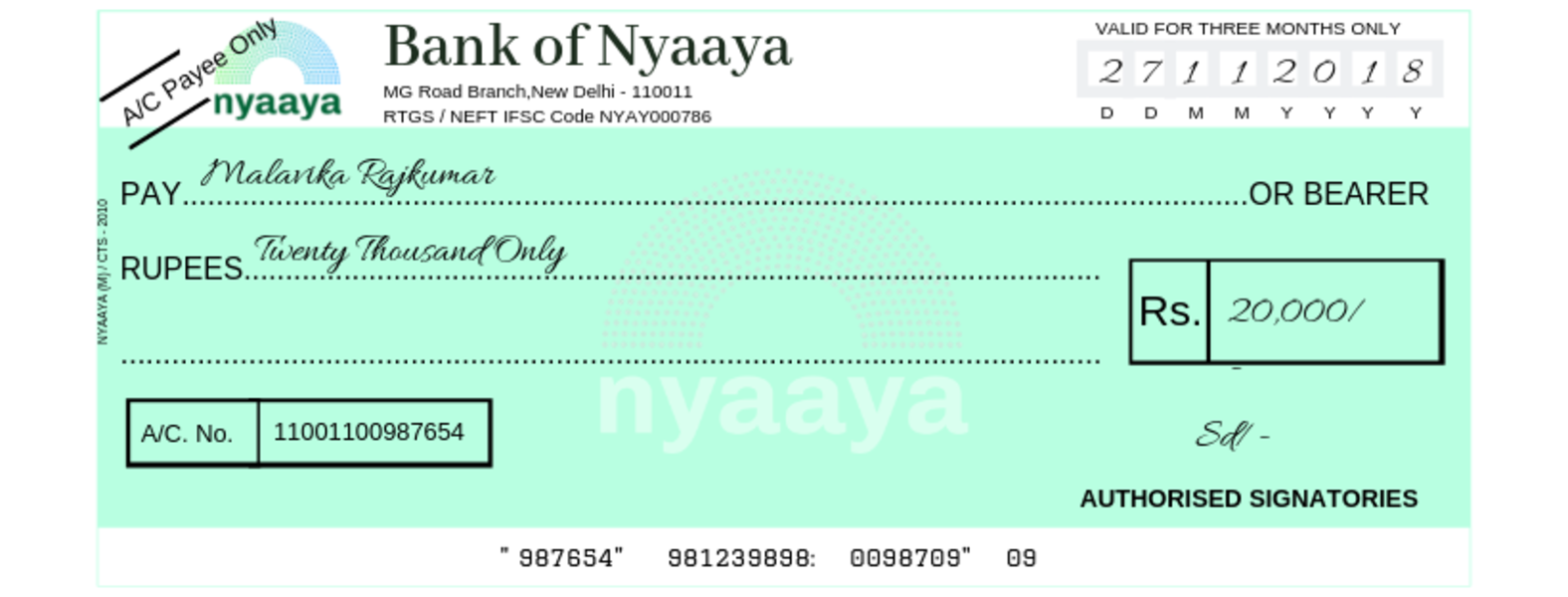

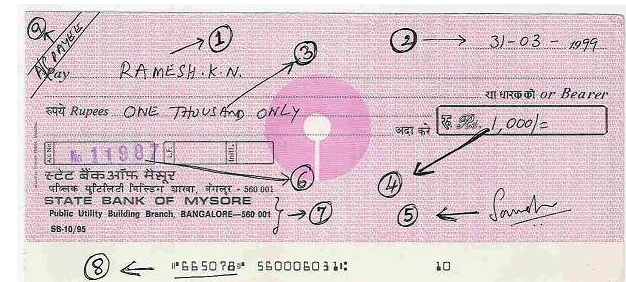

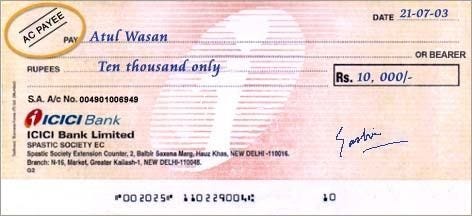

(C) Cheque

Drawer: Account holder

Drawee: Bank

Payee: Recipient

Other Important Parties

Holder (Section 8)

Person entitled to possession and to receive amount.

Holder in Due Course (Section 9)

Acquires instrument:

For consideration

Before maturity

In good faith

Gets better title.

Endorser / Endorsee

Endorser: Transfers instrument

Endorsee: Receives it

Legal Representative

Entitled upon death of holder.

3. Presentment of Negotiable Instruments

Meaning

Formal presentation of instrument for:

Acceptance (Bill of Exchange)

Payment (All instruments)

Types of Presentment

Presentment for Acceptance (Sections 61–69)

Required for:

Bills payable after sight

Must be made to drawee.

Presentment for Payment (Sections 64–77)

Necessary to charge parties (especially drawer/endorser).

Rules of Presentment

Must be made:

At proper place

During business hours

On due date

When Presentment is Not Necessary

Drawee prevents presentment

Party waives it

Impossible circumstances

4. Discharge of Parties

Modes of Discharge

By Payment (Section 82)

Payment in due course discharges all parties.

By Cancellation

Intentional cancellation of instrument.

By Release

Holder releases a party.

By Material Alteration (Section 87)

Without consent → instrument void.

By Negotiation Back

Instrument returns to prior party.

By Operation of Law

Insolvency, limitation, merger.

Discharge of One Party

Does not necessarily discharge others (unless principal debtor discharged).

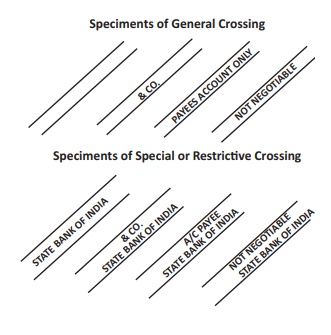

5. Crossing of Cheques (Sections 123–131)

Meaning

Crossing means drawing two parallel lines across cheque directing payment through a bank.

Kinds of Crossing

1. General Crossing (Section 123)

Two parallel lines

May include “& Co.”

Payment only through bank

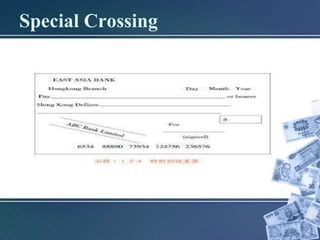

2. Special Crossing (Section 124)

Specifies a particular bank

Payment only to that bank

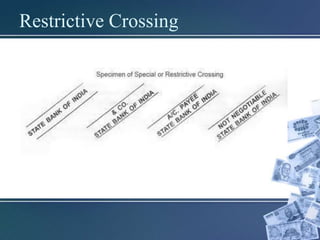

3. Restrictive Crossing (A/C Payee)

“Account Payee Only”

Cannot be further negotiated

4. Not Negotiable Crossing

Title of transferee defective if transferor had defective title

Effects of Crossing

Enhances security

Reduces misuse

Directs mode of payment

6. Rights of Holder & Holder in Due Course

Rights of Holder

To sue in own name

To receive amount

To endorse

To present for payment

Rights of Holder in Due Course

Better Title (Sec 53)

Even if previous title defective

Privilege Against Defects

Free from prior defects

Inchoate Instruments (Sec 20)

Can recover full amount

Estoppel (Sections 120–122)

Parties cannot deny validity

Distinction

| Basis | Holder | Holder in Due Course |

|---|---|---|

| Consideration | Not necessary | Necessary |

| Title | May be defective | Always better |

| Protection | Limited | Extensive |

7. Dishonour of Cheques

Types

Dishonour by Non-Payment

Dishonour by Non-Acceptance (for bills)

8. Civil Liability for Dishonour

Right to file civil suit for recovery

Based on:

Contract

Debt

9. Criminal Liability – Section 138

Essentials of Offence

Cheque drawn for discharge of debt/liability

Presented within validity period

Dishonoured due to:

Insufficient funds

Exceeds arrangement

Notice within 30 days

Failure to pay within 15 days

Punishment

Imprisonment up to 2 years, or

Fine up to twice the cheque amount, or both

Presumptions

Presumption of debt (Section 139)

Important Case Laws

K.N. Beena v. Muniyappan

Presumption under Section 139 is mandatory.

Rangappa v. Sri Mohan

Presumption includes existence of legally enforceable debt.

Dashrath Rupsingh Rathod v. State of Maharashtra

Territorial jurisdiction clarified.

10. Defences in Cheque Dishonour

No legally enforceable debt

Cheque issued as security

Material alteration

Notice not properly served

Conclusion

The Negotiable Instruments Act ensures:

Certainty in commercial transactions

Credibility of financial instruments

Legal remedies (civil & criminal)

It balances:

Ease of transferability

Protection against fraud and dishonour

Comments

Post a Comment